ESOPs and DAFs: A Strategic Combination for Business Owners Planning Their Next Chapter

As more business owners near retirement, many are seeking exit strategies that preserve their legacy, reward their employees, and create opportunities to give back. One increasingly attractive solution is combining an Employee Stock Ownership Plan (ESOP) with a donor-advised fund (DAF).

This powerful pairing can help clients achieve financial, personal, and philanthropic goals while maximizing tax advantages. The key to success? Early planning.

ESOPs: Preserving Legacy and Empowering Employees

ESOPs are gaining traction among founders planning succession. More than 6,500 ESOPs in the U.S. now benefit nearly 14 million employee-owners. These qualified retirement plans allow business owners to sell all or part of their company to employees, often preserving the business’s independence and promoting an ownership culture.

ESOPs also offer significant tax advantages. Under IRC Section 1042, eligible owners who sell to an ESOP can defer capital gains tax by reinvesting proceeds into qualified replacement property (QRP). QRP is defined as debt or equity instruments of domestic operating businesses, publicly or privately held. If held until death, QRP can be passed on to heirs with a step-up in basis, thereby eliminating capital gains tax liability.

What’s more, ESOPs offer flexibility. Owners can sell gradually, retaining a stake and control as they transition leadership and deepen employee ownership over time. For founders who want to phase out while reinforcing company culture, an ESOP can offer a path forward.

Incorporating Philanthropy with a Donor-Advised Fund

For clients with philanthropic goals, integrating a DAF into an ESOP transaction can be a strategic way to convert business equity into charitable capital.

By contributing closely held shares to a DAF before the ESOP sale, business owners may:

- Claim a fair market value charitable deduction.

- Avoid capital gains tax on the donated shares. For owners in the top federal tax bracket, capital gains tax savings can preserve up to 23.8% more value for giving, compared to selling the same shares outright and donating the after-tax proceeds.

- Establish a charitable fund with investment potential and administrative simplicity.

A DAF also offers ongoing flexibility: clients can support any qualified 501(c)(3) public charity, remain anonymous if they choose and engage family members in their philanthropy by appointing them as joint, secondary or successor DAF advisors. For business owners who care deeply about their communities, a DAF can help extend their philanthropic impact well beyond the sale of their business.

The table below outlines what an ESOP exit might look like, its benefits and who it is right for.

| Strategy | Structure | Key Benefits | Ideal For |

|---|---|---|---|

| Traditional ESOP Sale | 100% sale to ESOP | Maximum liquidity, full employee ownership | Owners seeking a clean exit |

| ESOP + DAF | 90% ESOP sale + 10% DAF gift | Reduced taxes, philanthropic capital | Philanthropically minded owners |

| ESOP + Sec. 1042 + DAF | 90% ESOP sale with 1042 rollover + 10% DAF gift | Tax deferral plus charitable impact | Philanthropically minded owners also focused on tax optimization |

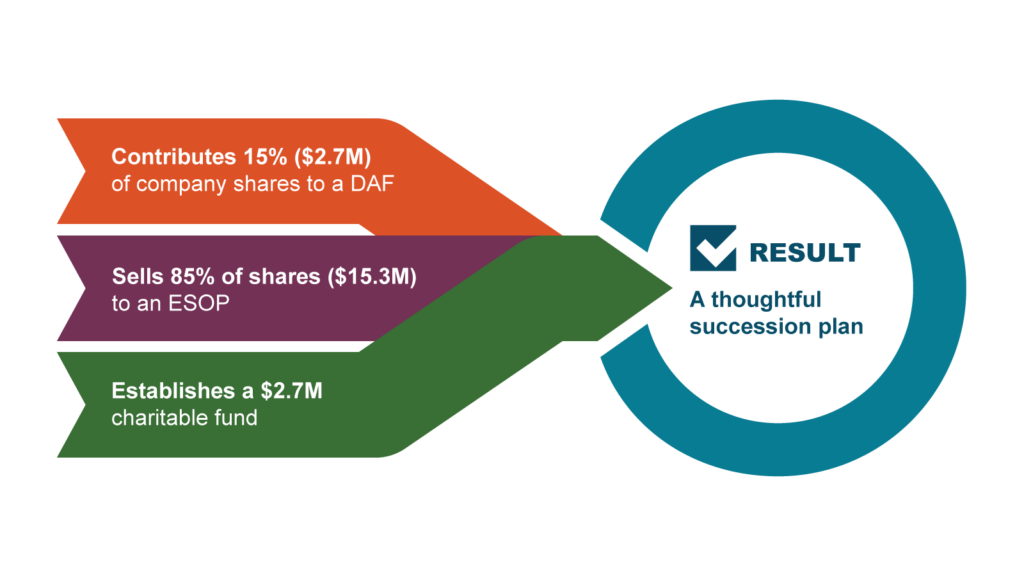

An Illustrative Example

Consider an owner of a successful manufacturing company planning to retire. The business is valued at $18 million, with a cost basis of $1.5 million. She wants to reward long-term employees, avoid selling to private equity and increase support for local education nonprofits.

Working with her advisor, she takes the following steps:

Contributes 15% of company shares ($2.7M) to a DAF

- Claims a charitable deduction at fair market value

- Avoids approximately $589,000 in capital gains tax*

Sells 85% of shares ($15.3M) to an ESOP

- Reinvests in QRP to achieve portfolio diversification; if held until death, the QRP receives a step up in basis

- Defers approximately $3.34M in capital gains tax* under IRC Section 1042

Establishes a $2.7M charitable fund

- Recommends DAF investments for potential growth

- Begins a grantmaking strategy focused on education

- Involves her children in recommending future grants

The result: a thoughtful succession plan that preserves the company’s culture, empowers employees, and sets aside significant capital for philanthropy.

Planning Matters

To fully capture the tax benefits of this strategy, timing is critical. Charitable contributions of closely held stock must be made before a binding agreement for the sale of owner shares to the ESOP is in place. Advisors should encourage clients to initiate planning well in advance.

NPT’s regional directors and philanthropic specialists can work alongside you and your clients’ advisory team to structure these gifts effectively, model outcomes, and develop a customized giving strategy that aligns with the client’s long-term goals.

To explore how an ESOP and DAF strategy may benefit your clients, contact us for a consultation.

*This hypothetical example assumes a capital gains rate of 23.8%, inclusive of a 3.8% NIIT. It also assumes the business interests have been held for longer than one year. Finally, this sample calculation assumes no valuation discounts.

About the Author

Rudy Flesher is Regional Director, West at National Philanthropic Trust (NPT). As a Regional Director, he cultivates relationships with financial advisors in Southern California and Arizona, providing consultative support to help clients achieve their philanthropic goals. He is based in Los Angeles, CA.

NPT is not affiliated with any of the organizations described herein, and the inclusion of any organization in this material should not be considered an endorsement by NPT of such organization, or its services or products.

NPT does not provide legal or tax advice. This blog post is for informational purposes only and is not intended to be, and shall not be relied upon as, legal or tax advice. The applicability of information contained here may vary depending on individual circumstances.