Integrating Donor-Advised Funds Across the Client Lifecycle

Donor-advised funds can help advisors integrate charitable giving into each stage of a client’s financial life.

For many advisors and donors, philanthropic planning still follows a familiar rhythm. It tends to surface late in the year, often as part of a broader discussion about tax efficiency, when timelines are compressed and decisions feel urgent. Donor-advised funds (DAFs) are introduced in this context as a practical solution to secure a deduction, manage giving, and move forward quickly.

This approach works. But it is inherently reactive. Treating DAFS only as a year-end solution overlooks their broader role in long-term philanthropic planning.

DAFs are among the most flexible and widely used giving vehicles, capable of supporting a range of strategies — from contributing complex assets to facilitating multigenerational philanthropy. Their value is not confined to a single moment in time. It builds when they are introduced earlier, revisited often, and aligned with the broader arc of a client’s financial life.

In practice, the difference comes down to timing. When philanthropic conversations move beyond the calendar and begin to follow the natural progression of a client’s life, DAFs begin to function less like tools of convenience and more like instruments of long-term planning.

Where Philanthropic Conversations Begin

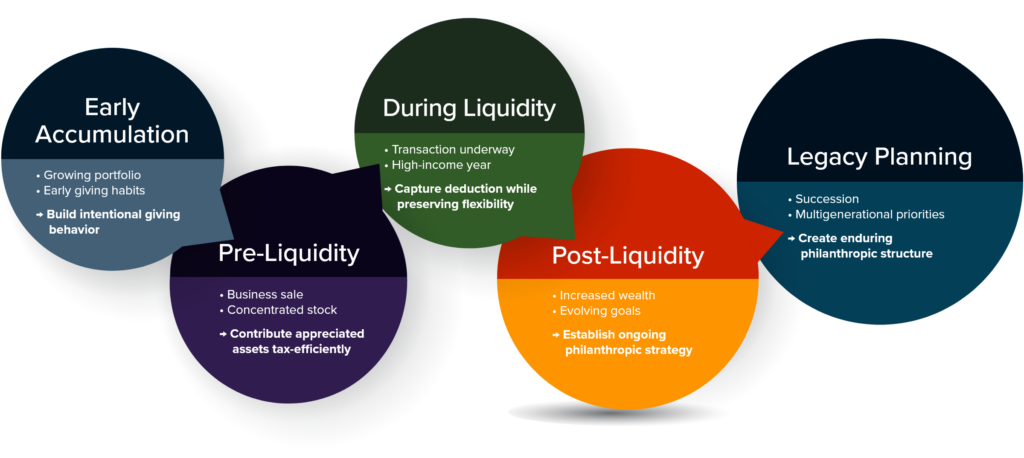

Philanthropic conversations can begin at several key stages in a client’s financial life.

Those inflection points are not difficult to identify. They appear in moments when change is already underway:

- A growing investment portfolio

- A concentrated position that has appreciated

- The early conversations around a business sale

- The arrival of new wealth

- The shift toward thinking about legacy and family.

Consider a client in the early stages of accumulation. Philanthropy may not yet be central to their financial plan, but patterns are already forming. They may give occasionally writing checks to organizations they care about or responding to requests on an ad hoc basis. The advisor’s role here is not to introduce complexity, but to introduce structure.

A DAF can provide a simple starting point for philanthropy: a structure through which appreciated securities can be contributed tax-efficiently, to consolidate giving, and to begin separating the act of contributing from the act of granting.

The amounts may be modest, but the behavior takes root. Giving becomes intentional rather than incidental.

Philanthropic Planning Throughout a Liquidity Event

A liquidity event, such as the sale of a business or another transaction that converts an asset into cash, can create philanthropic planning opportunities before, during, and after the transaction. The role of a DAF can evolve at each stage as a client’s financial circumstances and giving priorities change.

Exploring Philanthropic Options Before a Liquidity Event

Before a liquidity event, clients may have more options for aligning financial and philanthropic outcomes.

A different kind of conversation tends to emerge as clients approach a liquidity event. It may begin quietly, with an offhand comment about exploring a sale, a shift in how a client talks about their business, or a recognition that a concentrated position has reached a level where diversification is under consideration. What distinguishes this moment is not urgency, but opportunity. These conversations are often most effective when financial advisors, tax professionals, attorneys, and philanthropic specialists are aligned early and before transaction timelines narrow the available philanthropic planning options.

Take the example of a founder preparing to sell a closely held business. With thoughtful planning, a portion of shares can be contributed to a DAF before the transaction closes. Those shares are then sold within the DAF, allowing the donor to avoid capital gains on that portion. Depending on the asset type and transaction structure, that planning may involve coordination around valuation, due diligence, transfer timing, and sponsoring organization acceptance capabilities. The result is not only meaningful tax savings but also a larger pool of charitable capital than might otherwise have been available.

The result is not simply efficiency. It is an expansion of giving capacity at a moment when wealth is being reshaped.

The distinction is critical. Before a liquidity event, the conversation is about how to position assets in a way that can optimize both financial and philanthropic outcomes. Afterward, that opportunity may be significantly reduced.

During Liquidity: Acting Within the Moment

Not every client engages at this stage. In many cases, the conversation does not happen until the transaction is already in motion or even completed. At that point, the dynamic changes. The advisor is no longer structuring possibilities ahead of time but helping the client respond in real time.

In these moments — an executed options exercise, a completed sale, a year of unexpectedly high income — a DAF offers a different kind of value. It becomes a mechanism for capturing intent within a defined window. A client may not yet know which organizations they want to support or how they want to structure their giving, but they do know they want to act. Contributing to a DAF allows them to secure the tax benefit in the current year while giving themselves the space to make decisions more deliberately.

This separation between when a contribution is made and when grants are distributed is one of the defining advantages of the DAF structure. It introduces time when there might otherwise be pressure.

After Liquidity: Sustaining Engagement

And yet, even here, the work is not complete. In fact, in many ways, it is just beginning.

After liquidity, the urgency subsides. What remains is a new landscape: increased wealth, expanded capacity for giving, and often a less defined sense of what comes next.

This is where advisors have an opportunity to shift the conversation again.

They can help clients build a rhythm around giving. That may mean establishing a regular cadence for grantmaking, introducing new areas of interest, or involving family members in the process. A client who initially contributed to a DAF as part of a transaction may, over time, begin to see it as something more dynamic: a platform for exploration, decision-making, and participation.

For example, a recently retired business owner might begin inviting their adult children into the conversation, reviewing potential grants together and discussing the causes that matter most to them as a family. What began as a single contribution becomes an ongoing practice, one that evolves with time and perspective.

From Strategy to Legacy

As clients move further along in their financial journey, these conversations often take on additional meaning. Philanthropy becomes more closely tied to questions of legacy: not just how much to give, but how to give in a way that reflects values, engages future generations, and endures beyond the original donor.

Here again, DAFs offer both flexibility and structure. They can incorporate succession plans, designate future advisors, and serve as a vehicle for continued family involvement. More importantly, they provide a shared space where financial decisions and personal priorities intersect.

A Shift in Timing (and in Perspective)

Across each of these moments — from early accumulation to legacy planning — the common thread is not the tool itself, but the timing of its introduction. The same DAF can function very differently depending on when and how it enters the conversation. It can be a simple repository for year-end giving, or it can be a central component of a broader philanthropic strategy.

For advisors, it means recognizing that philanthropic conversations do not need to wait for December. They can begin when a portfolio takes shape, when an asset appreciates, when a transaction is contemplated, or when a client begins to ask different kinds of questions about the purpose of their wealth.

When those conversations happen earlier and continue over time, the outcomes tend to change. Giving becomes less reactive, more intentional, and more closely integrated with the rest of the planning process.

The result is not only more effective philanthropy, but a deeper and more enduring connection between financial decisions and the impact they are intended to create.

About the Author

Meghan Clifford is the Regional Director covering the Northeast. With over 20 years in the donor advised fund space, Meghan is dedicated to building relationships across the philanthropic landscape.

National Philanthropic Trust does not provide legal or tax advice. This material is for informational purposes only. The applicability of these strategies will vary based on individual circumstances, and readers of this communication should contact their lawyer to obtain advice with respect to any legal or tax matter.