Why the Donor-Advised Fund Payout Rate Matters and How It Fits Into the Bigger Picture

Those of us who work with donor-advised fund (DAF) donors every day see that they are caring, committed and creative givers. We know that they use DAFs for both their long- and short-term giving. This has never been more apparent than in the past year, when grantmaking from DAFs skyrocketed in response to the COVID-19 pandemic. While generosity is not a calculation, the DAF payout rate is an important benchmark in philanthropic activity.

What is the DAF payout rate?

The DAF payout rate is a calculation of grantmaking dollars from DAFs to charities relative to the total charitable assets in DAFs. More simply phrased: it’s how much DAF donors granted compared with what they could have granted.

How should we calculate payout rate?

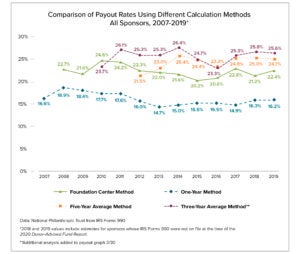

The Foundation Center uses a formula to estimate payout from private foundations, which NPT replicates in our annual Donor-Advised Fund Report. The Foundation Center method is:

This year’s grant $ ÷ Last year’s charitable assets $ = payout rate

For 2019, the latest aggregated year on record, the applied formula is:

FY19 grants ÷ FY18 charitable assets

or $27.37B ÷ $122.18B = 22.4% payout

NPT uses the Foundation Center method for several reasons. First, like DAFs, private foundations are widely used giving vehicles for both short- and long-term philanthropy, so using this method creates a useful point of comparison between the two types of vehicles. Second, the formula is not just the industry standard, it is practical. The Foundation Center method reflects common budgeting techniques—plan for the current year based on the prior year’s activity and any remaining balance and income. Third, other payout rate formulas ignore certain practical and particular aspects of giving to and from DAFs, like the time between the date of contribution and the availability of the funds for grantmaking. More on this last point below.

A look at other ways to calculate payout rate

Since there is no mandatory payout requirement for DAFs, there are several reasonable ways to calculate it. See below for a comparative chart.

The “Three-Year Average” and “Five-Year Average” methods use the average of the charitable assets held by DAFs over two different periods. These formulas are also allowed by the IRS as a way for private foundations to calculate their payout. Using multi-year averages can smooth out any “lumpiness” in either major contributions or grants. However, for fast-growing vehicles like DAFs, it also generally underestimates charitable assets available as the highest year—usually the most recent—is averaged with lower values from other years.

The “One-Year” method is a formula that NPT used to calculate DAF payout in our annual Donor-Advised Fund Report prior to 2014. The “One-Year” formula uses grants and charitable assets (plus grants) in the same year to calculate payout. This formula assumes that every dollar contributed to a DAF can be immediately granted out, which can have the effect of overestimating the value of assets that are truly available for grantmaking. For example, a donor who contributes to her DAF in the last days of December (and receives her tax deduction at that time) will recommend grants from those DAF charitable assets the following year and beyond.

How do we put the DAF payout rate into context?

The Foundation Center method offers the best point of comparison. Private foundations are similar giving vehicles to DAFs, and this method most accurately represents payout by using numbers that reflect the amount granted relative to what is definitively available for grantmaking.

It is also worth noting that private foundation payouts can include eligible operating and administrative expenses, like the foundation’s staff, overhead and accounting. By contrast, DAF payout is strictly charitable grantmaking and does not include any of the DAF sponsors’ operating or administrative expenses.

Using the Foundation Center method, DAF payout is typically at least four times higher than that of private foundations. While foundations typically grant out the legally required minimum of 5% of their assets annually, the DAF payout rate has been above 20% for each of the last 10 years. Perhaps more significantly though, all of the proposed formulae show that the DAF payout rate is historically and consistently higher than private foundations. The DAF payout rate helps us understand that DAF donors are committed to the charities they support in both the long- and short-term.

DAFs provide substantial and sustained support

A consistent DAF payout rate is good news for charities. DAF donors have proven that they are a sustainable source of charitable support. They give dependably across economic cycles (yes, DAF donors still gave at a 20+ % payout rate through the Great Recession); through political seasons (no, there’s no need to worry that campaign giving decreases charitable giving for DAF donors); and in the face of great challenges (natural disasters, global pandemics, mass social movements and otherwise). The data is clear: DAF donors are committed to the long-term viability of nonprofits.

The DAF payout rate is an important metric, but it’s not the only way to measure philanthropic activity from DAF donors. Grantmaking from DAFs has nearly doubled in the last five years—a clear signal that DAF donors are active philanthropists. In fact, growth in grantmaking from DAFs has outpaced growth in contributions to them in the last five years, growing 93% and 80% respectively. DAF donors’ response to the COVID-19 global pandemic—when DAF grantmaking soared 33% year-over-year—is yet another indication of their philanthropic commitment. So is the fact that they have irrevocably donated money to DAFs, which can only be used for philanthropic purposes. While there is no magic formula to make people give, DAF donors have consistently chosen to do so generously.

NPT does not provide legal or tax advice. This blog post is for informational purposes only and is not intended to be, and shall not be relied upon as, legal or tax advice. The applicability of information contained here may vary depending on individual circumstances.

To download a PDF of this blog post, click below:

![]()

![]()

About the Author

Andrew Hastings is NPT’s Executive, Family Office & Private Client Development. He has 30 years of experience in the philanthropic and nonprofit marketplace. He is responsible for advancing NPT’s work with family offices, founders and entrepreneurs.